Canada Gazette, Part I, Volume 153, Number 43: By-law Amending the Canada Deposit Insurance Corporation Differential Premiums By-law

October 26, 2019

Statutory authority

Canada Deposit Insurance Corporation Act

Sponsoring agency

Canada Deposit Insurance Corporation

REGULATORY IMPACT ANALYSIS STATEMENT

(This statement is not part of the By-law.)

Background

The Board of Directors of the Canada Deposit Insurance Corporation (CDIC) made the Canada Deposit Insurance Corporation Differential Premiums By-law (By-law) on March 3, 1999, pursuant to subsection 21(2) and paragraph 11(2)(g) of the Canada Deposit Insurance Corporation Act (CDIC Act). Subsection 21(2) of the CDIC Act authorizes the CDIC Board of Directors to make by-laws establishing a system of classifying member institutions into different categories, setting out the criteria or factors the CDIC will consider in classifying members into categories, establishing the procedures the CDIC will follow in classifying members, and fixing the amount of, or providing a manner of determining the amount of, the annual premium applicable to each category. The CDIC Board of Directors amended the By-law on January 12 and December 6, 2000, July 26, 2001, March 7, 2002, March 3, 2004, February 9 and April 15, 2005, February 8 and December 6, 2006, December 3, 2008, December 2, 2009, December 8, 2010, December 7, 2011, December 5, 2012, December 4, 2013, April 22, 2015, February 4 and December 7, 2016, December 6, 2017, December 5, 2018, and March 6, 2019.

Issues

The CDIC annually reviews the By-law to confirm it is technically up to date. As a result, technical amendments are proposed to the By-law Amending the Canada Deposit Insurance Corporation Differential Premiums By-law (the Amending By-law). Furthermore, the By-law has been reviewed to eliminate redundancies. The Amending By-law primarily targets the following two main issues:

1. Changes to the Reporting Form

The amendments align the By-law with the changes in the Office of the Superintendent of Financial Institutions (OSFI) forms that are referenced in the By-law. Furthermore, the amendments seek to remove redundancies in the Reporting Form where formulas are found elsewhere in the By-law or correspond to OSFI data points found in the Reporting Manual. It also removes the scoring grids from the Reporting Form, as they are contained in other parts of the By-law.

2. Clarification to and simplification of existing requirements

The amendments correct the calculation of the score in a situation where there is no examiner’s rating component and simplifies the calculation of the capital adequacy score component. Amendments also clarify that if the Corporation adjusts the Reporting Form, it will use the adjusted Reporting Form when assigning scores under other sections of the By-law.

Description

The tables below provide more detail about the amendments proposed in the Amending By-law.

| Amending By-law Section | By-law Section | Explanation |

|---|---|---|

| [1] | 1(1) | Amendments align the definition of "Reporting Manual" with the terminology used by OSFI. |

| [2] | 20(2) | Amendments clarify that if the Corporation adjusts the Reporting Form, it will use the adjusted Reporting Form when assigning scores under other sections of the By-law. |

| [3] | 21 | Consequential amendments resulting from proposed amendments to simplify the inputs to the capital adequacy measures contained in Schedule 2. |

| [4] | 28(3) | Amendments correct the manner in which the score for the examiner’s rating is to be assigned in a situation where no examiner rating is available to the Corporation and correct references to other sections of the By-law. |

| Amending By-law Section | By-law Section | Explanation |

|---|---|---|

| [5] | Item 1 | Amendment simplifies the calculation of the score for the capital adequacy measures by directly referring to the data point that is available through OSFI reporting. |

| [6] | Item 2 | Amendments update the formula to remove the reference to Tier 1 capital, which reflects the changes made to Schedule 1 of the Basel Capital Adequacy Reporting form. |

| [7, 8, 9 and 10] | Items 3, 4, 5 and 6 | Amendments remove the scoring grids that pertain to the mean adjusted net income volatility measure, the stress-tested net income measure, the efficiency ratio measure, and the net impaired assets to total capital measure, as sufficient clarity in respect of scoring for those measures appears in Schedule 3 of the By-law. |

| [11(1) and (2)] | Item 7 | Amendments align wording with that used in the OSFI forms. |

| [11(3)] | Item 7 | Amendment removes the scoring grid that pertains to the three-year moving average asset growth measure, as it is redundant and sufficient clarity in respect of scoring for that measure appears in Schedule 3 of the By-law. |

| [12] | Item 8 | Amendments align wording with that used in the OSFI forms and ensure calculations provide outcome prior to subtracting for allowance for expected credit losses. |

| [13(1) and (2)] | Item 8-1 | Amendments align wording with that used in the OSFI forms and clarify the required calculation. |

| [13(3)] | Item 8-1 | Amendment removes the scoring grid that pertains to the asset encumbrance measure, as it is redundant and sufficient clarity in respect of scoring for that measure appears in Schedule 3 of the By-law. |

| [14] | Item 9 | Amendment removes the scoring grid that pertains to the aggregate commercial loan concentration ratio measure, as it is redundant and sufficient clarity in respect of scoring for that measure appears in Schedule 3 of the By-law. |

| [15] | Item 10 | Amendment removes the calculation of the total quantitative score, as the calculation of the total quantitative score is appropriately detailed in Schedule 3 of the By-law. |

| Amending By-law Section | By-law Section | Explanation |

|---|---|---|

| [16] | Item 2, column 3 | Amendment corrects the scoring grid to account for the scenario where the Tier 1 capital ratio ≥ the minimum Tier 1 capital ratio required by the regulator. |

“One-for-One” Rule

The “One-for-One” Rule does not apply to this proposal, as there is no change in administrative costs to business.

Small business lens

The small business lens does not apply to this proposal, as there are no costs to small business.

Alternatives

There are no available alternatives. The amendments must be done by way of by-law.

Consultation

As the amendments are technical in nature and do not affect the substantive elements of the By-law, only consultation by way of prepublication in the Canada Gazette, Part I, is necessary.

Rationale

The proposed Amending By-law will ensure the By-law remains technically up to date, will achieve the stated objective, and addresses the identified issues. The Amending By-law would not impose any additional regulatory costs or administrative burden on industry.

Implementation, enforcement and service standards

The proposed Amending By-law would come into effect for the 2020 premium year. There are no compliance or enforcement issues.

Contact

Noah Arshinoff

Manager

Insurance

Canada Deposit Insurance Corporation

50 O’Connor Street, 17th Floor

Ottawa, Ontario

K1P 6L2

Telephone: 613‑995‑6548

Email: narshinoff@cdic.ca

PROPOSED REGULATORY TEXT

Notice is given that the Board of Directors of the Canada Deposit Insurance Corporation, pursuant to subsection 21(2) footnote a of the Canada Deposit Insurance Corporation Act footnote b, proposes to make the annexed By-law Amending the Canada Deposit Insurance Corporation Differential Premiums By-law.

Interested persons may make representations concerning the proposed By-law within 30 days after the date of publication of this notice. All such representations must cite the Canada Gazette, Part I, and the date of publication of this notice, and be addressed to Noah Arshinoff, Manager, Insurance, Canada Deposit Insurance Corporation, 50 O’Connor Street, 17th Floor, Ottawa, Ontario K1P 6L2 (email: narshinoff@cdic.ca).

Ottawa, October 8, 2019

Peter Routledge

President and Chief Executive Officer

Canada Deposit Insurance Corporation

By-law Amending the Canada Deposit Insurance Corporation Differential Premiums By-law

Amendments

1 The definition Reporting Manual in subsection 1(1) of the Canada Deposit Insurance Corporation Differential Premiums By-law footnote 1 is replaced by the following:

- Reporting Manual means the Manual of Reporting Forms and Instructions published for deposit-taking institutions by the Superintendent, as amended from time to time. (Recueil des formulaires et des instructions)

2 Subsection 20(2) of the By-law is replaced by the following:

(2) If the Corporation makes an adjustment to the Reporting Form under subsection (1), it shall use the adjusted Reporting Form for the purpose of assigning scores under sections 21 to 27.

3 Section 21 of the By-law is replaced by the following:

21 The Corporation shall assign to each member institution the sum of the scores set out in columns 2 and 4 of Part 1 of Schedule 3 that correspond, respectively, to the descriptions set out in columns 1 and 3 of that Part that apply to the results obtained for that institution in respect of elements 1.1 to 1.5 of item 1 of the Reporting Form.

4 Subsection 28(3) of the By-law is replaced by the following:

(3) If none of the examiner’s ratings referred to in subsection (2) are available to the Corporation for the member institution, the score to be assigned for the purposes of that subsection shall be the result determined in accordance with the formula

(A ÷ 60) × 35

where

- A is the sum of the scores assigned to the member institution under sections 21 to 27.

| 1 CAPITAL ADEQUACY MEASURES |

|---|

| Refer to the Leverage Requirements Return (LRR) and Basel III Capital Adequacy Reporting – Credit, Market and Operational Risk (BCAR) form, Reporting Manual, completed in accordance with that Manual as of the end of the fiscal year ending in the year preceding the filing year. |

1.1 Leverage Ratio (%) Indicate the leverage ratio (%) as set out in Section 1 – Leverage Ratio Calculation of the LRR. 1.1% |

1.2 Authorized Leverage Ratio (%) Indicate the authorized leverage ratio (%) as set out in Section 1 – Leverage Ratio Calculation of the LRR. 1.2% |

1.3 Tier 1 Capital Ratio (%) Indicate the Tier 1 capital ratio (%) as set out in Schedule 1 – Ratio Calculations of the BCAR form. 1.3% |

1.4 Minimum Tier 1 Capital Ratio Indicate the minimum Tier 1 capital ratio as set by the regulator for the member institution in accordance with the Capital Adequacy Requirements guideline of the Guidelines, but if a different minimum Tier 1 capital ratio has been set by the regulator by written notice sent to the member institution, indicate that ratio instead. 1.4% |

1.5 "All in" Target Tier 1 Capital Ratio Indicate the "all in" target Tier 1 capital ratio (including the capital conservation buffer and domestic systemically important bank surcharge as applicable) as set by the regulator for the member institution in accordance with the Capital Adequacy Requirements guideline of the Guidelines, but if a different "all in" target Tier 1 capital ratio has been set by the regulator by written notice sent to the member institution, indicate that ratio instead. 1.5% |

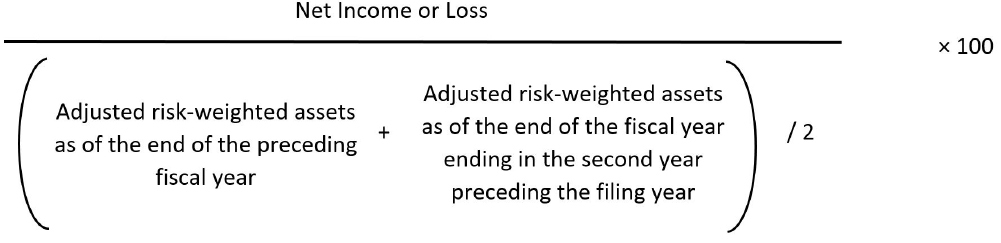

6 (1) The formula under the heading “Formula:” in item 2 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

Image description

Multiply by 100 the result of the following: net income or loss divided by the result of dividing by 2 the sum of the adjusted risk-weighted assets as of the end of the preceding fiscal year and the adjusted risk-weighted assets as of the end of the fiscal year ending in the second year preceding the filing year.

2.2 Adjusted Risk-Weighted Assets as of the End of the Fiscal Year Ending in the Year Preceding the Filing Year Indicate the adjusted risk-weighted assets as set out in Schedule 1 – Ratio Calculations of the BCAR form. |

2.3 Adjusted Risk-Weighted Assets as of the End of the Fiscal Year Ending in the Second Year Preceding the Filing Year Indicate the adjusted risk-weighted assets as of the end of the fiscal year ending in the second year preceding the filing year, calculated in the same manner as for element 2.2. If the member institution does not have a fiscal year ending in the second year preceding the filing year, it must indicate "zero", unless it is an amalgamated institution described below. If the member institution is an amalgamated member institution formed by an amalgamation involving one or more member institutions and does not have a fiscal year ending in the second year preceding the filing year, it must indicate the same amount as for element 2.2. |

7 The portion of item 3 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 4 is repealed.

8 The portion of item 4 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 5 is repealed.

9 The portion of item 5 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 6 is repealed.

10 The portion of item 6 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 7 is repealed.

11 (1) The paragraph after the heading “7.4.7 Total derivative contract exposure (not covered)” in item 7 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

Indicate the amount set out in the column “Total Contracts” for “(A) Single derivative exposure not covered by an eligible netting contract, (i) Replacement cost”, as set out in Section 2 – Derivative Exposure Calculation of the LRR.

(2) The paragraph after the heading “7.4.8 Total derivative contract exposure (covered)” in item 7 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

Indicate the amount set out in the column “Total Contracts” for “(B) Derivative exposure covered by an eligible netting contract, (i) Replacement cost”, as set out in Section 2 – Derivative Exposure Calculation of the LRR.

(3) The portion of item 7 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 8 is repealed.

12 (1) The second paragraph under the heading “Elements” in item 8 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

Refer to the Mortgage Loans Report, the Non-Mortgage Loans Report and Section I – Assets of the Consolidated Monthly Balance Sheet, Reporting Manual, all completed in accordance with that Manual as of the end of the fiscal year ending in the year preceding the filing year.

(2) The paragraph after the heading “8.1 Total Mortgage Loans” in item 8 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

The total mortgage loans is the sum of the amounts set out in the column “Total” under “Total Mortgage Loans” and “Less allowance for expected credit losses” in Section I of the Mortgage Loans Report.

(3) The paragraph after the heading “8.2 Total Non-Mortgage Loans” in item 8 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

The total non-mortgage loans is the sum of the amounts set out for “Total” in the columns “TC” under “Resident Loan Balances” and “Non-Resident Loan Balances” in the Non-Mortgage Loans Report.

(4) The portion of item 8 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 8-1 is repealed.

13 (1) The second paragraph under the heading “Elements” in item 8-1 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

Refer to the Consolidated Monthly Balance Sheet, the Return of Allowances for Expected Credit Losses and Section I of the Pledging and Repos Report, Reporting Manual, all completed in accordance with that Manual as of the end of the fiscal year ending in the year preceding the filing year.

(2) The paragraph after the heading “8-1.1.8 Impairment” in item 8-1 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law is replaced by the following:

Impairment is the amount set out for “Total” in the column “Recorded Investment Total” under “Stage III”, less the aggregate of the amounts set out for “Total” in the columns “Expected Credit Losses” under “Stage I”, “Stage II” and “Stage III”, in the Return of Allowances for Expected Credit Losses.

(3) The portion of item 8-1 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 9 is repealed.

14 The portion of item 9 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law beginning with the heading “Score” and ending before item 10 is repealed.

15 Item 10 of the Reporting Form set out in Part 2 of Schedule 2 to the By-law ending before “The information provided in this Reporting Form is based on:” is repealed.

| Item | Column 3 Tier 1 Capital Ratio |

|---|---|

| 2 | Tier 1 capital ratio is ≤ the "all in" target Tier 1 capital ratio set by the regulator for the member institution but ≥ the minimum Tier 1 capital ratio required by the regulator |

Coming into Force

17 This By-law comes into force on the day on which it is registered.