Vol. 151, No. 21 — October 18, 2017

Registration

SOR/2017-216 October 5, 2017

CANADIAN ENVIRONMENTAL PROTECTION ACT, 1999

Regulations Amending the Ozone-depleting Substances and Halocarbon Alternatives Regulations

P.C. 2017-1226 October 5, 2017

Whereas, pursuant to subsection 332(1) (see footnote a) of the Canadian Environmental Protection Act, 1999 (see footnote b), the Minister of the Environment published in the Canada Gazette, Part I, on November 26, 2016, a copy of the proposed Regulations Amending the Ozone-depleting Substances and Halocarbon Alternatives Regulations, substantially in the annexed form, and persons were given an opportunity to file comments with respect to the proposed Regulations or to file a notice of objection requesting that a board of review be established and stating the reasons for the objection;

Whereas, pursuant to subsection 93(3) of that Act, the National Advisory Committee has been given an opportunity to provide its advice under section 6 (see footnote c) of that Act;

And whereas, in accordance with subsection 93(4) of that Act, the Governor in Council is of the opinion that the proposed Regulations do not regulate an aspect of a substance that is regulated by or under any other Act of Parliament in a manner that provides, in the opinion of the Governor in Council, sufficient protection to the environment and human health;

Therefore, Her Excellency the Governor General in Council, on the recommendation of the Minister of the Environment and the Minister of Health, pursuant to subsection 93(1) of the Canadian Environmental Protection Act, 1999 (see footnote d), makes the annexed Regulations Amending the Ozone-depleting Substances and Halocarbon Alternatives Regulations.

Regulations Amending the Ozone-depleting Substances and Halocarbon Alternatives Regulations

Amendments

1 Section 4 of the Ozone-depleting Substances and Halocarbon Alternatives Regulations (see footnote 1) is amended by striking out “or” at the end of paragraph (b), by adding “or” at the end of paragraph (c) and by adding the following after paragraph (c):

- (d) an automobile that is in transit through Canada from a place outside Canada to another place outside Canada.

2 Subsection 34(1) of the English version of the Regulations is amended by striking out “or” at the end of paragraph (b) and by replacing paragraph (c) with the following:

- (c) its use as feedstock; or

- (d) any other purpose that complies with the laws of the importing Party.

3 Paragraph 42(3)(a) of the French version of the Regulations is replaced by the following:

- a) aux soins des personnes ou des animaux, y compris les dilatateurs de bronches, les stéroïdes pris par inhalation, les anesthésiques topiques et les vaporisateurs de poudre utilisée en médecine vétérinaire sur les blessures;

4 The heading before section 55 of the Regulations is replaced by the following:

Consumption Allowances for HCFCs

5 Paragraphs 55(2)(a) and (b) of the French version of the Regulations are replaced by the following:

- a) s’agissant d’une cession permanente, pour chacune des années civiles suivant celle de la cession;

- b) s’agissant d’une cession temporaire, seulement pour l’année civile en cause.

6 Subsection 56(2) of the Regulations is replaced by the following:

Calculated level of consumption

(2) The calculated level of consumption for an HCFC — excluding a recovered, recycled or reclaimed HCFC that is imported or exported — that is manufactured, imported or exported during a calendar year must be determined using the following formula:

(M × ODP) + (I × ODP) – (E × ODP) – (Di × ODP)

- where

- M is the quantity manufactured during the calendar year, other than the quantity manufactured for use as feedstock;

- ODP is the ozone-depleting potential set out in column 2 of Table 3 of Schedule 1 for the HCFC in question;

- I is the quantity imported during the calendar year;

- E is the quantity exported during the calendar year; and

- Diis the quantity imported during the calendar year for destruction under paragraph 54(1)(a).

7 The heading before section 60 of the Regulations is replaced by the following:

Manufacturing Allowance for HCFCs

8 Subsection 60(2) of the Regulations is replaced by the following:

Greater manufacturing allowance

(2) When it is necessary to allow Canada to fulfill its obligations under an agreement with a Party for the purpose of industrial rationalization or to satisfy domestic HCFC needs, the Minister may permit, for a calendar year, a greater manufacturing allowance than that which a person would have obtained under subsection (1) and that greater manufacturing allowance is not taken into account in any subsequent calculation of the annual manufacturing allowance.

Written notice

(3) The Minister must inform the person in writing of their manufacturing allowance.

9 Subsection 61(2) of the Regulations is replaced by the following:

Calculated level of manufacture

(2) The calculated level of manufacture for an HCFC must be determined using the following formula:

(M × ODP) – (Dm × ODP)

- where

- M is the quantity manufactured during the calendar year, other than the quantity manufactured for use as feedstock;

- ODP is the ozone-depleting potential set out in column 2 of Table 3 of Schedule 1 for the HCFC in question; and

- Dmis the quantity manufactured during the calendar year for destruction under paragraph 54(1)(a).

10 Section 62 of the Regulations is repealed.

11 (1) Sections 64 and 65 of the Regulations are replaced by the following:

Prohibition — importing HFCs without permit

64 It is prohibited for any person to import an HFC set out in Table 4 of Schedule 1 without a permit issued under these Regulations.

Purpose of importing

64.1 (1) The permit may only be issued to import an HFC for one of the following purposes:

- (a) its destruction;

- (b) its use as feedstock; or

- (c) a use for which a substance set out in Tables 1 to 3 of Schedule 1 has been used in Canada.

Importing regardless of purpose

(2) A permit may also be issued to import, regardless of purpose, an HFC that is recovered, recycled or reclaimed.

Exception — consumption allowance

64.2 Section 64 does not apply to a person who is granted an annual consumption allowance for an HFC or a transferee of an annual consumption allowance for an HFC intended for a use for which a substance set out in Tables 1 to 3 of Schedule 1 has been used in Canada.

Refillable container

64.3 Any HFC that is imported for use as a refrigerant must be stored in a refillable container.

Importing Products Containing HFCs

Prohibition — importing certain products containing HFCs used as refrigerants

64.4 (1) As of the date indicated in column 3 of Schedule 1.1, it is prohibited for any person to import any product set out in that Schedule that contains or is designed to contain an HFC that is set out in Table 4 of Schedule 1 and is to be used as a refrigerant, if the global warming potential of the refrigerant used in that product is greater than the specified limit in Schedule 1.1.

Exception — personal effect

(2) Subsection (1) does not apply to a product set out in Schedule 1.1 that is destined for residential use if it is a personal effect of the person.

Automobiles — 2021 and subsequent model years

(3) Beginning with the 2021 model year, it is prohibited for any person to import an automobile equipped with an air-conditioning system that contains or is designed to contain an HFC that is set out in Table 4 of Schedule 1 and is to be used as a refrigerant if the global warming potential of the refrigerant used in that system is greater than 150.

Exception — personal use automobile

(4) Subsection (3) does not apply to an automobile destined for the person’s personal use.

Plastic foam or rigid foam product

64.5 (1) As of January 1, 2021, it is prohibited for any person to import a plastic foam or a rigid foam product in which an HFC set out in Table 4 of Schedule 1 is used as a foaming agent if the global warming potential of the foaming agent is greater than 150.

Exception — personal effect

(2) Subsection (1) does not apply to a person’s personal effect that contains a plastic foam or a rigid foam product.

Exception — military, space or aeronautical applications

(3) Subsection (1) does not apply to a plastic foam or a rigid foam product that is intended to be used for military, space or aeronautical applications.

Pressurized containers — 2 kg or less of HFC used as propellant

64.6 (1) As of January 1, 2019, it is prohibited for any person to import a pressurized container that contains 2 kg or less of an HFC when the HFC is used as a propellant if the global warming potential of that HFC is greater than 150.

Exceptions — miscellaneous products

(2) Subsection (1) does not apply to a pressurized container that contains

- (a) a mould release agent or mould cleaning agent;

- (b) a spinneret lubricant or cleaning agent used in the manufacture of synthetic fibers;

- (c) a document preservation agent;

- (d) a lubricant, cleaning agent, freezing agent or corrosion prevention agent used for electrical equipment or electronic components;

- (e) a duster agent used on photographic negatives and semiconductor chips;

- (f) a lubricant, cleaning agent or corrosion prevention agent used for aircraft maintenance;

- (g) a pesticide used near electrical wires or in aircraft or a certified organic-use pesticide;

- (h) a stench gas used in mines; or

- (i) a cooling agent used for testing electronics and electro-mechanical systems.

Exception — health care products and laboratory or analytical use

(3) Subsection (1) does not apply to a pressurized container that contains a product that is intended

- (a) for use in animal or human health care, including a bronchial dilator, inhalable steroid, topical anaesthetic, bandage adhesive remover and veterinary wound powder spray; or

- (b) for a laboratory or analytical use.

Manufacture of HFCs

Prohibition — manufacture of HFCs without permit

65 It is prohibited for any person to manufacture an HFC set out in Table 4 of Schedule 1 without a permit issued under these Regulations.

Purpose of manufacture

65.01 The permit may only be issued to manufacture an HFC to be used as feedstock.

Prohibition — manufacturing products containing HFCs used as refrigerants

65.02 (1) As of the date indicated in column 3 of Schedule 1.1, it is prohibited for any person to manufacture any product set out in that Schedule that contains or is designed to contain an HFC set out in Table 4 of Schedule 1 and used as a refrigerant if the global warming potential of the refrigerant used in that product is greater than the limit specified in Schedule 1.1.

Automobiles — 2021 and subsequent model years

(2) Beginning with the 2021 model year, it is prohibited for any person to manufacture an automobile equipped with an air-conditioning system that contains or is designed to contain an HFC that is set out in Table 4 of Schedule 1 and is to be used as a refrigerant if the global warming potential of the refrigerant used in that system is greater than 150, unless it is intended to be exported.

Plastic foam or rigid foam product

65.03 (1) As of January 1, 2021, it is prohibited for any person to manufacture a plastic foam or a rigid foam product in which an HFC set out in Table 4 of Schedule 1 is used as a foaming agent if the global warming potential of the foaming agent is greater than 150.

Exception — military, space or aeronautic applications

(2) Subsection (1) does not apply to a plastic foam or a rigid foam product that is intented to be used for military, space or aeronautical applications.

Pressurized containers — 2 kg or less of an HFC used as propellant

65.04 (1) As of January 1, 2019, it is prohibited for any person to manufacture a pressurized container that contains 2 kg or less of an HFC when the HFC is used as a propellant if the global warming potential of that HFC is greater than 150.

Exception — miscellaneous products

(2) Subsection (1) does not apply to the pressurized containers referred to in subsections 64.6(2) and (3).

Destruction of HFCs

HFC no longer needed

65.05 A person in possession of an HFC set out in Table 4 of Schedule 1 that was imported or manufactured under a permit issued under these Regulations and that is no longer needed for the use set out in that permit must, within six months after the day on which it is no longer needed,

- (a) ensure that it is sent for destruction to a facility referred to in paragraph 12(c);

- (b) ensure that it is exported for destruction, for use as feedstock or for a laboratory or analytical use; or

- (c) in the case of a recovered, recycled or reclaimed HFC, ensure that it is sent to a recycling or reclamation facility.

Consumption Allowance for HFCs

Calculation of consumption allowance for HFCs

65.06 (1) The annual consumption allowance for an HFC set out in Table 4 of Schedule 1 to which a person is entitled is determined as follows:

- (a) for each calendar year that falls within the period that begins on January 1, 2019 and ends on December 31, 2023, by multiplying the base consumption granted to that person by 90%;

- (b) for each calendar year that falls within the period that begins on January 1, 2024 and ends on December 31, 2028, by multiplying the base consumption granted to that person by 60%;

- (c) for each calendar year that falls within the period that begins on January 1, 2029 and ends on December 31, 2033, by multiplying the base consumption granted to that person by 30%;

- (d) for each calendar year that falls within the period that begins on January 1, 2034 and ends on December 31, 2035, by multiplying the base consumption granted to that person by 20%; and

- (e) as of January 1, 2036, by multiplying the base consumption granted to that person by 15%.

Calculation of base consumption

(2) The base consumption granted to a person is determined as follows:

C/D × E

- where

- C is the person’s average HFC consumption for 2014 and 2015, expressed in tonnes of CO2 equivalent;

- D is the average Canadian HFC consumption for 2014 and 2015, expressed in tonnes of CO2 equivalent; and

- E is 19 118 651 tonnes of CO2 equivalent.

Permanent or temporary transfer

(3) If a transfer of a portion of the consumption allowance is approved in accordance with subsection 65.08(4), the transferred portion is subtracted from or added to the person’s annual consumption allowance, as the case may be,

- (a) in the case of a permanent transfer, for every calendar year following the year of the transfer; and

- (b) in the case of a temporary transfer, for the calendar year of the transfer.

Written notice

(4) The Minister must inform the person in writing of their consumption allowance.

Annual consumption allowance for HFCs not to be exceeded

65.07 (1) A person who is granted an annual consumption allowance must ensure that it is not exceeded by determining their calculated level of consumption for each HFC for a calendar year and then adding together all of their calculated levels of consumption.

Calculated level of consumption

(2) The calculated level of consumption for an HFC — excluding a recovered, recycled or reclaimed HFC that is imported or exported — that is manufactured, imported or exported during a calendar year must be determined using the following formula:

(M × GWP) + (I × GWP) – (E × GWP)

- where

- M is the quantity manufactured during the calendar year, other than the quantity manufactured for use as feedstock;

- GWP is the global warming potential of the HFC;

- I is the quantity imported during the calendar year; and

- E is the quantity exported during the calendar year.

Prohibition — transfer without authorization

65.08 (1) It is prohibited for any person to transfer all or a portion of their annual consumption allowance of HFCs unless the Minister approves the transfer under subsection (4).

Temporary or permanent transfer

(2) A transfer is temporary if it applies to only one calendar year and it is permanent if it applies to all calendar years.

Application to Minister

(3) The transferor and transferee must submit an application for the transfer to the Minister that contains the information required by Schedule 4 and specifies whether the proposed transfer is temporary or permanent.

Conditions

(4) The Minister must approve the transfer if the transferor has an unused consumption allowance that is not less than the quantity of the proposed transfer.

Written notice

(5) The Minister must inform the transferor and transferee in writing of the decision concerning the application for a transfer and of their consumption allowances.

Grounds for refusal and cancellation

65.09 (1) The Minister may refuse to approve or may cancel a transfer if the Minister has reasonable grounds to believe that the transferee is not able to manufacture, use, sell, import or export an HFC in compliance with Canadian law.

Effect of cancellation

(2) If the Minister cancels a transfer, the transferee must, without delay, transfer back to the transferor any unused portion of the consumption allowance.

Retirement of consumption allowances

65.1 (1) A person may retire their consumption allowance by providing the Minister with a notice in writing to that effect containing the information required by Schedule 4.

Effect of retirement

(2) A person who has retired their consumption allowance is not entitled to any further consumption allowance.

(2) Paragraph 64.1(1)(c) of the Regulations is repealed.

12 Subsection 66(1) of the Regulations is replaced by the following:

Exceptions — essential purpose

66 (1) Despite subsection 13(1), sections 15 and 17, subsection 19(1), sections 40 and 41, subsections 42(1) and 43(1), sections 48 and 49, subsection 50(1), section 51, subsection 53(1), subsections 64.4(1), 64.5(1) and 64.6(1), sections 65.02 and 65.03 and subsection 65.04(1), a person may import, manufacture, use or sell a substance set out in Table 1, 3 or 4 of Schedule 1 or a product containing or designed to contain that substance if the substance or product will be used for an essential purpose and if a permit is specifically issued under these Regulations for that purpose.

13 Section 70 of the Regulations is replaced by the following:

Duration

70 (1) A permit is effective

- (a) if the application is submitted for the current year, for the period beginning on the date of its issuance and ending on December 31 of the year in which it is issued; or

- (b) if the application is submitted for the subsequent year, for the period beginning on January 1 and ending on December 31 of the year for which it is issued.

Essential purpose

(2) Despite subsection (1), a permit for an essential purpose may be issued for a period of up to 36 months.

14 (1) Schedule 1 to the Regulations is amended by replacing the references after the heading “SCHEDULE 1” with the following:

(Paragraph 3(a), section 5, paragraph 6(1)(c), section 8, subsection 9(1), section 10, paragraph 11(1)(b), subsection 13(1), sections 14 to 18, subsection 19(1), paragraphs 19(2)(b), 22(c), 24(b) and 32(b), sections 33, 35 and 36, paragraph 37(1)(b), section 41, subsections 42(1) and 43(1), sections 44, 45 and 49, subsection 50(1), sections 51 and 52, subsections 53(1), 54(1), 55(1), 56(2), 60(1) and 61(2), sections 63 and 64, paragraph 64.1(1)(c), section 64.2, subsections 64.4(1) and (3) and 64.5(1), sections 65 and 65.02, subsection 65.03(1), section 65.05 and subsections 65.06(1), 66(1) and 75(2))

(2) Schedule 1 to the Regulations is amended by replacing the references after the heading “SCHEDULE 1” with the following:

(Paragraph 3(a), section 5, paragraph 6(1)(c), section 8, subsection 9(1), section 10, paragraph 11(1)(b), subsection 13(1), sections 14 to 18, subsection 19(1), paragraphs 19(2)(b), 22(c), 24(b) and 32(b), sections 33, 35 and 36, paragraph 37(1)(b), section 41, subsections 42(1) and 43(1), sections 44, 45 and 49, subsection 50(1), sections 51 and 52, subsections 53(1), 54(1), 55(1), 56(2), 60(1) and 61(2), sections 63, 64 and 64.2, subsections 64.4(1) and (3) and 64.5(1), sections 65 and 65.02, subsection 65.03(1), section 65.05 and subsections 65.06(1), 66(1) and 75(2))

15 Table 4 of Schedule 1 to the Regulations is replaced by the following:

TABLE 4

Part 4 Substances

| Item |

Column 1 |

Column 2 |

|---|---|---|

1 |

HFCs: |

|

(a) Trifluoromethane (HFC-23) |

14 800 |

|

(b) Difluoromethane (HFC-32) |

675 |

|

(c) Fluoromethane (HFC-41) |

92 |

|

(d) 1,1,1,2,2-pentafluoroethane (HFC-125) |

3 500 |

|

(e) 1,1,2,2-tetrafluoroethane (HFC-134) |

1 100 |

|

(f) 1,1,1,2-tetrafluoroethane (HFC-134a) |

1 430 |

|

(g) 1,1,2-trifluoroethane (HFC-143) |

353 |

|

(h) 1,1,1-trifluoroethane (HFC-143a) |

4 470 |

|

(i) 1,2-difluoroethane (HFC-152) |

53 |

|

(j) 1,1-difluoroethane (HFC-152a) |

124 |

|

(k) 1,1,1,2,3,3,3-heptafluoropropane (HFC-227ea) |

3 220 |

|

(l) 1,1,1,2,2,3-hexafluoropropane (HFC-236cb) |

1 340 |

|

(m) 1,1,1,2,3,3-hexafluoropropane (HFC-236ea) |

1 370 |

|

(n) 1,1,1,3,3,3-hexafluoropropane (HFC-236fa) |

9 810 |

|

(o) 1,1,2,2,3-pentafluoropropane (HFC-245ca) |

693 |

|

(p) 1,1,1,3,3-pentafluoropropane (HFC-245fa) |

1 030 |

|

(q) 1,1,1,3,3-pentafluorobutane (HFC-365mfc) |

794 |

|

(r) 1,1,1,2,2,3,4,5,5,5-decafluoropentane (HFC-43-10mee) |

1 640 |

16 The Regulations are amended by adding, after Schedule 1, the Schedule 1.1 set out in the schedule to these Regulations.

17 Schedule 4 to the Regulations is amended by replacing the references after the heading “SCHEDULE 4” with the following:

(Subsections 57(3), 59(1), 65.08(3) and 65.1(1))

18 The heading of Schedule 4 to the Regulations is replaced by the following:

Application for a Transfer of a Consumption Allowance for HCFCs or HFCs and Notice Retiring an Allowance — Information Required

19 Subparagraph 1(b)(ii) of Schedule 4 to the Regulations is replaced by the following:

- (ii) the quantity of HCFCs or HFCs to be transferred.

20 (1) Paragraph 2(c) of Schedule 5 to the English version of the Regulations is replaced by the following:

- (c) information respecting the source of the product: the name, civic and postal addresses, telephone number and, if any, email address and fax number of the manufacturer;

(2) The portion of paragraph 2(d) of Schedule 5 to the English version of the Regulations before subparagraph (i) is replaced by the following:

- (d) information respecting the destination of the product:

Coming into Force

180 days after publication

21 (1) These Regulations, except subsections 11(2) and 14(2), come into force on the 180th day after the day on which they are published in the Canada Gazette, Part II.

January 1, 2019

(2) Subsections 11(2) and 14(2) come into force on January 1, 2019.

SCHEDULE

(Section 16)

SCHEDULE 1.1

(Subsections 64.4(1) and (2) and 65.02(1))

Products Containing or Designed to Contain an HFC Used as a Refrigerant

| Item |

Column 1 |

Column 2 |

Column 3 |

Column 4 |

|---|---|---|---|---|

1 |

Stand-alone medium-temperature refrigeration system: self-contained refrigeration system with components that are integrated within its structure and that is designed to maintain an internal temperature ≥ 0°C |

(a) Commercial or industrial |

January 1, 2020 |

1 400 |

(b) Residential |

January 1, 2025 |

150 |

||

2 |

Stand-alone low-temperature refrigeration system: self-contained refrigeration system with components that are integrated within its structure and that is designed to maintain an internal temperature < 0°C but < -50°C |

(a) Commercial or industrial |

January 1, 2020 |

1 500 |

(b) Residential |

January 1, 2025 |

150 |

||

3 |

Centralized refrigeration system: refrigeration system with a cooling evaporator in the refrigerated space connected to a compressor rack located in a machinery room and to a condenser located outdoors, and that is designed to maintain an internal temperature at ≥ -50°C |

Commercial or industrial |

January 1, 2020 |

2 200 |

4 |

condensing unit: refrigeration system with at a cooling evaporator in the refrigerated space connected to a compressor and condenser unit that are located in a different location, and that is designed to maintain an internal temperature at ≥ -50°C |

Commercial or industrial |

January 1, 2020 |

2 200 |

5 |

chiller: refrigeration or air-conditioning system that has a compressor, an evaporator and a secondary coolant, other than an absorption chiller |

Commercial or industrial |

January 1, 2025 |

750 |

6 |

mobile refrigeration system: refrigeration system that is normally attached to or installed in, or operates in or with a means of transportation |

Commercial or industrial |

January 1, 2025 |

2 200 |

REGULATORY IMPACT ANALYSIS STATEMENT

(This statement is not part of the regulations.)

Executive summary

Issues: Hydrofluorocarbons (HFCs) are chemicals widely used in refrigeration and air-conditioning equipment and foam manufacturing. They are also greenhouse gases (GHGs), and short-lived climate pollutants (SLCPs), most with global warming potentials hundreds to thousands of times more potent than carbon dioxide (CO2). GHG emissions are contributing to a global warming trend associated with climate change. Without immediate action, annual GHG emissions from HFCs in Canada are projected to increase from 9 megatonnes (Mt) CO2-equivalent (CO2e) in 2014 to 19 Mt in 2030.

Description: The Regulations Amending the Ozone-depleting Substances and Halocarbon Alternatives Regulations (the Amendments) will control HFCs through the phase-down of consumption of bulk HFCs complemented by controls on specific products containing or designed to contain HFCs, including refrigeration and air-conditioning equipment, foams and aerosols. (see footnote 2)

Cost-benefit statement: Between 2018 and 2040, the Amendments are expected to result in cumulative GHG emission reductions from HFCs of about 168 Mt CO2e. The benefits of these GHG emission reductions are valued at about $6.2 billion. Compliance costs incurred by industry are estimated at almost $2.2 billion, which are partially offset by related cost savings of almost $48 million. The net benefit of the Amendments is estimated to be about $4 billion (in present value terms, discounted at 3% per year to 2017).

“One-for-One” Rule and small business lens: The Amendments will result in a net decrease in average annual administrative burden costs of around $1,100, or about $60 per business per year. The Amendments are therefore considered to be an “OUT” under the Government of Canada’s “One-for-One” Rule.

The small business lens applies and, after industry consultations, various flexibilities were incorporated into the Amendments to address the concerns of small businesses. These flexibilities are expected to reduce the cost of the proposal for small business, relative to the initial option considered, by $9.8 million, or $980 000 per small business over 23 years.

Domestic and international coordination and cooperation: The Amendments are consistent with the October 2016 Kigali Amendment to the Montreal Protocol and put Canada in a position to ratify this amendment. The Amendments are also consistent with Canada’s commitments under the Pan-Canadian Framework on Clean Growth and Climate Change, in which Canada resolved to implement its commitment under the Paris Agreement, to take action to reduce HFC use and emissions. The Amendments complement existing provincial and territorial measures, which aim to minimize and reduce HFC emissions from existing equipment.

Background

Hydrofluorocarbons (HFCs) are manufactured chemicals that were introduced on the global market as replacements for ozone-depleting substances, such as chlorofluorocarbons (CFCs) and hydrochlorofluorocarbons (HCFCs). HFCs are not manufactured in Canada, but are imported in bulk and found in imported and manufactured products, such as domestic appliances, refrigeration and air-conditioning systems, motor vehicle air-conditioning systems, foam products, and aerosols. HFCs enter the environment due to leakage during assembly, usage, and disposal of these products. (see footnote 3)

Although HFCs are not ozone-depleting and have proven to be suitable cost efficient alternatives for ozone-depleting substances they replace, they are (like many CFCs and HCFCs) potent greenhouse gases (GHGs) with global warming potentials hundreds to thousands of times greater than carbon dioxide (CO2). (see footnote 4)

GHG emissions are contributing to a global warming trend that is associated with climate change, which is projected to lead to both changes in average conditions and in extreme weather events. The impacts of climate change are expected to become more negative as the global average surface temperature becomes increasingly warmer. Climate change impacts are of major concern for society: changes in temperature and precipitation can impact natural habitats, agriculture and food supplies, and rising sea levels can threaten coastal communities. (see footnote 5)

Most HFCs are Short-lived Climate Pollutants (SLCPs) that have a relatively short lifespan in the atmosphere compared to CO2 and other longer-lived GHGs. Atmospheric levels of HFCs thus respond relatively quickly to changes in emissions since they are removed quickly from the atmosphere. As a result of the potency and short lifespan of HFCs, reducing emissions has the potential to bring significant near-term climate benefits. Canada is committed to reducing HFC emissions both domestically and by supporting international actions, including as a founding member of the Climate and Clean Air Coalition, an international voluntary initiative aimed at improving air quality and protecting the climate by reducing SLCPs, including HFCs.

The Montreal Protocol

The Montreal Protocol on Substances that Deplete the Ozone Layer (Montreal Protocol) is an international treaty designed to protect the ozone layer. Originally signed by Canada in 1987, the Montreal Protocol obligates Parties to phase out the manufacture and consumption of those substances known to be responsible for ozone depletion. The phase-out is achieved through a legally binding timetable established by the Parties with the ultimate goal of complete elimination. The Montreal Protocol is widely recognized as one of the most successful international environmental treaties, with significant reductions in ozone-depleting substances contributing to the expected recovery of the ozone layer by mid-century. In addition, given that many ozone-depleting substances are also potent greenhouse gases, the Montreal Protocol has, as a secondary accomplishment, contributed to climate change mitigation by averting the emissions of 135 billion tonnes of CO2e.

Current domestic measures

Canada’s obligations under the Montreal Protocol were implemented by the Ozone-Depleting Substances Regulations, 1998, which replaced three regulations controlling ozone-depleting substances and products containing them. The Ozone-Depleting Substances Regulations, 1998 phased out the manufacture and consumption of CFCs and HCFCs. As a first step to more comprehensive measures on HFCs, the Government of Canada introduced, in 2016, the Ozone-depleting Substances and Halocarbon Alternatives Regulations (the Regulations), which repealed and replaced the Ozone-Depleting Substances Regulations, 1998 and introduced a permitting and reporting system to monitor quantities of HFCs imported, manufactured, and exported, with reporting to begin in 2018 for activities that took place in the 2017 calendar year. (see footnote 6)

Currently, there are federal, provincial, and territorial regulations in place to limit emissions from existing equipment that use HFCs. These regulations include the Federal Halocarbon Regulations, 2003, which aim to minimize and reduce HFC emissions from equipment owned by the Crown or a federal work or undertaking or from equipment located on Aboriginal lands or federal lands. These regulations aim to reduce HFC emissions by requiring regular equipment maintenance and recovery of refrigerants during equipment maintenance and at end-of-life. These regulations do not control bulk HFCs. In addition, the provinces and territories are responsible for controlling the sale, handling, use, recovery and recycling of ozone-depleting substances and their halocarbon alternatives used in equipment that falls under their jurisdiction. Almost all Canadian provinces and territories have now implemented legislation for the recovery of ozone-depleting substances and HFCs. Notwithstanding these federal and provincial measures, the use of HFCs will still result in leakage from equipment and products that contain them.

In recognition of the risks of HFC use, a notice of intent was published in the Canada Gazette, Part I, in December 2014, announcing Canada’s intention to develop regulatory measures to control the manufacture, import, and use of HFCs. This notice affirmed Canada’s intention to align its measures with those of the United States, to the extent possible, and to continue to work with international partners to globally phase down HFCs. (see footnote 7)

International and domestic commitments

At the United Nations Framework Convention on Climate Change (UNFCCC) conference in December 2015, the international community, including Canada, adopted the Paris Agreement, an accord intended to reduce global greenhouse gas emissions with a long-term goal of limiting the rise in global average temperature to less than 2°C above pre-industrial levels and to aim to limit the increase to 1.5°C. As part of its Nationally Determined Contribution (NDC) commitment under the Paris Agreement, Canada pledged to reduce national GHG emissions by 30% below 2005 levels by 2030, including a commitment to gradually phase down HFCs. (see footnote 8) The Department of the Environment (the Department) currently estimates that annual emission reductions of 219 megatonnes (Mt) will be required in 2030 to deliver on this commitment. (see footnote 9)

In October 2016, Parties to the Montreal Protocol, including Canada, adopted an HFC phase-down amendment (the Kigali Amendment) wherein developed countries will begin in 2019 to gradually phase down HFCs to 15% of calculated baseline levels by 2036. Developing countries will take their first step to control HFCs in 2024 or 2028, phasing down to 15% or 20% of baseline levels by 2046.

On December 9, 2016, Prime Minister Trudeau, along with most first ministers of Canada, agreed to the Pan-Canadian Framework on Clean Growth and Climate Change (Pan-Canadian Framework). (see footnote 10) The Pan-Canadian Framework was developed to establish a path forward to meet Canada’s commitments under the Paris Agreement. Within the Pan-Canadian Framework, the Government of Canada committed to various climate actions, including regulatory measures to reduce HFC emissions.

Issues

GHG emissions, including HFCs and CO2, are contributing to a global warming trend that is associated with climate change. HFCs have global warming potentials hundreds to thousands of times greater than those of CO2. HFC emissions are projected to increase at a faster rate than economic growth due to increased use as they replace ozone-depleting substances that have been phased out under the Montreal Protocol. Without immediate action, annual HFC emissions in Canada are projected to increase from 9 Mt of CO2e emissions per year in 2014 to 19 Mt per year in 2030, which is underlining the significant need for action on HFCs.

Current measures do not control the import of bulk HFCs or the import and manufacture of equipment and products that contain HFCs. While measures are in place to limit emissions from HFC-containing products, they cannot eliminate all emissions that occur from leakage during the life cycle of these products.

Parties to the Montreal Protocol, including Canada, have adopted the Kigali Amendment to phase down the production and consumption of HFCs. In order to ratify the Kigali Amendment, the Department needs to put regulatory measures in place that will allow Canada to meet its obligations to phase down HFCs as set out in the aforementioned amendment.

Objectives

The Regulations Amending the Ozone-depleting Substances and Halocarbon Alternatives Regulations (the Amendments) aim to reduce the supply of HFCs that enter into Canada and the demand for HFCs in manufactured products, thereby averting future HFC releases to the environment. This will reduce Canadian GHG emissions, in order to help limit increases in global average temperatures and contribute to Canada’s international obligations to combat climate change. Additionally, the Amendments aim to allow Canada to ratify the Kigali Amendment to the Montreal Protocol.

Description

The Amendments

- control the amount of HFCs available for use through the phase-down of bulk HFCs;

- introduce controls on specific products containing HFCs, including air-conditioning and refrigeration equipment, foams and aerosols; and

- make minor modifications to the HCFC provisions in the Regulations.

These provisions will directly impact

- bulk importers of HFCs, who import HFCs in bulk quantities for sale to, or use by manufacturers;

- manufacturers of air-conditioning and refrigeration equipment, foams and aerosols; and

- one HCFC manufacturer.

Accompanying the Amendments are consequential amendments to the Regulations Designating Regulatory Provisions for Purposes of Enforcement (Canadian Environmental Protection Act, 1999) [Designation Regulations]. (see footnote 11) The Designation Regulations designate the various provisions of regulations made under the Canadian Environmental Protection Act, 1999 (CEPA) that are linked to a fine regime following the successful prosecution of an offence involving harm or risk of harm to the environment, or obstruction of authority. The Regulations are listed in the Designation Regulations, which will need to be amended to reflect the addition of new offences pertaining to the import, manufacture and export of HFCs (e.g. import of non-compliant products containing HFCs).

1. Phase-down of consumption of bulk HFCs

HFCs are commonly imported into Canada in bulk for use in the manufacture, servicing and maintenance of refrigeration and air-conditioning equipment, and in the manufacture of foam-blowing products. Reducing quantities of HFCs imported into Canada will encourage manufacturers of products containing HFCs to transition to alternative substances, as the supply of HFCs will decrease.

Under the Amendments, overall “baseline” levels of HFC consumption will be calculated using consumption (defined as the sum of quantities manufactured and imported minus quantities exported) of HFCs from 2011 to 2013, plus 15% of Canada’s HCFC consumption baseline (expressed in tonnes CO2e). All importers of bulk HFCs will receive an individual consumption allowance, which when added together will total Canada’s consumption baseline. These consumption allowances will be distributed based on the individual importer’s share of Canada’s total HFC consumption in 2014 and 2015. The Department collected this information through mandatory surveys conducted from 2014 through 2016. Following the phase-down schedule in the Amendments (see Table 1), the quantity of HFCs authorized for import under consumption allowances will decrease over time, while individual shares of this decreasing number will remain constant. Individual allowances could be partially or fully transferred to other parties, subject to the written approval of the Minister.

Table 1: Canada’s HFC consumption phase-down

| Year |

Reduction from Baseline (%) |

Canada’s Maximum Allowable HFC Consumption (tonnes CO2e) |

|---|---|---|

2019 |

10 |

17,206,786 |

2024 |

40 |

11,471,191 |

2030 |

70 |

5,735,595 |

2034 |

80 |

3,823,730 |

2036 |

85 |

2,867,798 |

Note: The baseline level of HFC consumption is 19,118,651 tonnes CO2e. |

||

HFCs contained in imported pre-charged equipment such as cars, air-conditioning systems, refrigeration systems and domestic appliances will not be included in the phase-down provisions, but will be subject to the product-specific controls.

2. Product-specific controls

The Amendments introduce product-specific controls that will prohibit the import and manufacture of products and equipment that contain or are designed to contain any HFC, or any blend that contains an HFC, with a global warming potential greater than the designated limit. The product-specific controls will apply to the refrigeration and air conditioning, foam, mobile air-conditioning, and aerosols sectors. Unique global warming potential (GWP) limits and prohibition dates will be applied to different product types within each sector.

The product-specific controls provide exceptions for a number of technical and medical aerosol products, such as certain cleaning products for electronics and metered-dose inhalers, for which alternatives do not yet exist. (see footnote 12) In addition, the Amendments will allow for exceptions, with the approval of the Minister of the Environment, if

- the product is necessary for health and safety or is critical for the good functioning of society; and

- there are no technically and economically feasible alternatives.

The Amendments will not prevent the use and sale of products manufactured or imported before the date of prohibition.

3. Minor HCFC amendments

The changes to the HCFC provisions include the introduction of measures that will allow Canada’s sole manufacturer of HCFCs to manufacture additional quantities of HCFCs when necessary to support other countries. These measures are consistent with the provisions in the Montreal Protocol and allow the Minister to track, via a permitting system, any such quantities produced. Changes also include corrections to the English version of one provision to ensure consistency between the English and the French versions of the regulatory text.

Notable changes from the proposed Amendments as published in the Canada Gazette, Part I (CG-I)

Of the above described elements of these Amendments, the following notable areas were revised after the publication of the proposed Amendments in CG-I:

- The determinants of the consumption allowance, such as phase-down schedule and base consumption calculations, were changed to align with the Kigali Amendment to the Montreal Protocol, which was adopted after publication in CG-I.

- The GWP threshold for stand-alone medium temperature refrigeration systems and centralized refrigeration systems was increased from 700 to 1 400 and 1 500 to 2 200, respectively; additionally, the threshold for chillers was increased from 700 to 750. These changes were made to allow for more replacement refrigerants to be used and to more closely align with U.S. measures.

- Exemptions were extended to include the import and manufacture of certain products containing HFCs for personal use; military, space or aeronautical applications; and automobiles that are subsequently destined for export.

- The definitions of centralized refrigeration system, condensing unit and chiller were changed to provide clarification of the intended systems targeted by the measures.

- Foam products were grouped into one category to minimize confusion due to overlap in foam categories.

Regulatory and non-regulatory options considered

With the coming into force of the Ozone-depleting Substances and Halocarbon Alternatives Regulations, the Government of Canada has begun regulating the manufacture and consumption of HFCs through the introduction of a permitting and reporting system; however, this system does not impose limits to the quantities of HFCs that can be consumed in Canada. The Government of Canada also seeks to minimize and reduce HFC emissions, through the Federal Halocarbon Regulations, 2003, from equipment owned by the Crown or a federal work or undertaking or from equipment located on Aboriginal or federal lands. Similar to these federal measures, provinces and territories have legislation in place that aims to minimize and reduce emissions of HFCs used in equipment under provincial/territorial jurisdiction. Other major industrialized countries have also enacted regulations to limit growth in emissions of HFCs and avoid future emissions. When considering how to address the public policy issue, the Government of Canada considered three options: maintaining the regulatory status quo; updating the regulatory requirements to control specific products; or implementing an approach with a phase-down of bulk HFCs, plus product-specific controls to increase GHG emission reductions and better align with similar U.S. measures.

Status quo approach

Without the Amendments, no measures will be in place to ensure reductions in HFC consumption in Canada, which is expected to increase in the future, as HFCs replace the ozone-depleting substances (such as HCFCs) currently being phased out. Although some reductions in HFC use may occur due to measures in other countries (e.g. measures in the United States may reduce HFC content in imported products), the Department anticipates the status quo approach would result in increasing HFC use, and a risk that Canada could become a dumping ground for products containing HFCs. Additionally, while federal and provincial measures are in place to limit emissions of HFC from equipment, they do not control the import, manufacture, export or use of HFCs and do not eliminate all HFC emissions. Given that the status quo approach would result in increased HFC use and emissions, contribute to global warming, and undermine Canada’s international obligations to combat climate change (Paris Agreement) and phase down HFC consumption (Kigali Amendment), this option was rejected.

Regulatory approach — Product-specific controls with no bulk HFC phase-down

In 2014, the Department proposed to take domestic action on HFCs through a notice of intent to align measures with those of the United States to the extent possible. The current U.S. approach, under the Significant New Alternatives Policy (SNAP) Program, prohibits the use of specific HFCs in certain end-use equipment/products, but does not include a phase-down. (see footnote 13) During consultations, stakeholders expressed a strong desire to include a phase-down component, in addition to the product-specific prohibitions outlined in the Notice of Intent. This approach is similar to the one used to successfully phase-out ozone-depleting substances such as CFCs and HCFCs in Canada. Further, excluding the phase-down would limit Canada’s potential GHG reductions under the Amendments. After these consultations took place, the Kigali Amendment was adopted by Parties to the Montreal Protocol, including Canada, thus committing the Government of Canada to implement a bulk HFC phase-down. In order to ensure Canada meets its international obligations and given stakeholder feedback, this option was rejected.

Regulatory approach — Product-specific controls plus bulk HFC phase-down

The Government of Canada has committed to reduce HFC use to avoid subsequent GHG emissions. Additionally, Canada has committed to phase-down HFC use under the Kigali Amendment. Thus, the Amendments will include a phase-down of bulk HFC consumption, allowing Canada to ratify the Kigali Amendment to the Montreal Protocol. In addition to ensuring Canada meets its international obligations, the phase-down will lead to meaningful GHG emission reductions.

The Amendments also include product-specific controls similar to those currently in place in the U.S. For the product-specific controls, the Amendments do not prescribe the specific HFCs prohibited or the alternatives allowed in each of the equipment and product types. Instead, the Amendments establish Global Warming Potential limits for a variety of products, and provide stakeholders flexibility on how best to comply. The Global Warming Potential limits are designed to allow for the same alternatives to be used in both Canada and the United States as well as prohibit the same HFCs, and will also prevent the introduction of high Global Warming Potential substitutes from being used. The timing of the introduction of product-specific HFC controls was designed to align with the timing of enacted measures in the U.S. to the extent possible. These approaches are based on consultation with industry regarding the availability of technologies and the implementation challenges.

Canada’s Amendments are also similar to regulatory controls implemented in the European Union and Japan, and the approach being considered by Australia, which include both a phase-down of HFCs and product-specific controls.

Benefits and costs

Between 2018 and 2040, the Amendments are expected to result in cumulative GHG emission reductions of about 168 Mt CO2e. The benefits of these GHG emission reductions are valued at about $6.2 billion. There will be compliance costs incurred by industry of about $2.2 billion, in addition to related cost savings of almost $48 million. The net benefits of the Amendments are estimated to be about $4 billion (in present value terms, discounted at 3% per year to 2017).

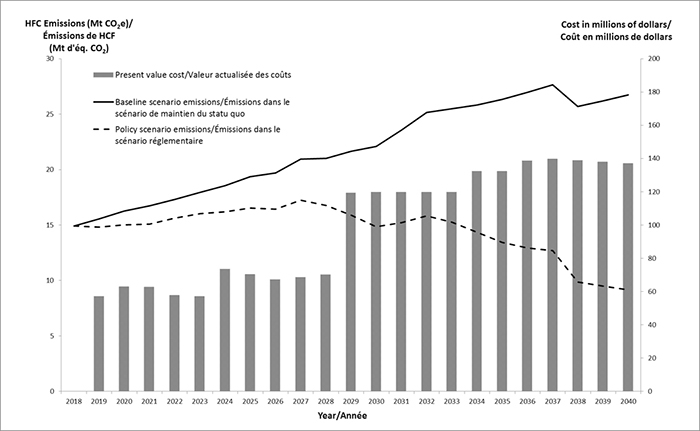

As shown in Figure 1 below, costs and benefits increase significantly post-2029 as the bulk phase-down schedule increases in stringency. While costs remain relatively constant post-2036, emission reductions continue to increase as the stock of in-service equipment still containing HFCs is retired over time.

Figure 1: Baseline and policy HFC emissions and compliance costs by year

Analytical framework

TBS guidance: The impacts of the Amendments have been assessed in accordance with the Treasury Board Secretariat (TBS) Canadian Cost-Benefit Analysis Guide. (see footnote 14) Regulatory impacts have been identified, quantified and monetized where possible, and compared incrementally to a non-regulatory scenario. The analysis has estimated these impacts over a sufficient time period to demonstrate whether there is likely to be a net benefit.

Key impacts: The key expected impacts of the Amendments are demonstrated in the logic model (Figure 2) below: a phase-down of HFC consumption, in addition to Global Warming Potential limits for certain HFC-containing products, will lead to the adoption of alternative substances with lower Global Warming Potential, resulting in decreased emissions of high Global Warming Potential HFCs. Compliance with the Amendments will also lead to capital and operating costs for industry, with associated cost savings for some firms as a result of the lower price of replacement substances.

Figure 2: Logic model for the analysis of the Amendments

Logic model for the analysis of the Amendments |

||||||||

|---|---|---|---|---|---|---|---|---|

Phase-down of bulk HFCs |

→ |

Reduction in supply of HFCs for use in products |

→ |

Adoption of low Global Warming Potential alternatives |

→ |

Reduction in emissions of high Global Warming Potential HFCs |

→ |

Reduction in climate change impacts |

→ |

Capital and operating costs |

|||||||

Global Warming Potential limits for certain products |

→ |

Increase in demand for HFC alternatives for use in products |

→ |

→ |

Net costs to industry |

|||

→ |

Operating cost savings |

|||||||

Comparative scenarios: The analysis compares the expected impacts of the Amendments (the regulatory scenario) to a non-regulatory scenario that assumes the Amendments are not implemented (the baseline scenario). This baseline scenario assumes that if the Amendments are not implemented, then HFC use in domestic manufacturing and servicing would remain unchanged relative to projected levels. The incremental impacts (benefits and costs) between the two scenarios are then attributed to the Amendments.

Time frame of analysis: The time frame considered for this analysis is 2018–2040. This time frame captures costs up to the point they reach their maximum value in 2037. GHG reductions are expected to increase beyond 2040, as the stock of equipment using HFCs is replaced with new equipment using low Global Warming Potential alternatives. Benefits exceed costs in any given year beyond 2021. Therefore, the 2018–2040 time frame was considered sufficient for estimating whether the proposal will result in a net benefit.

Monetary results: All monetary results are shown in 2016 Canadian dollars after inflating any prices that are not from 2016. (see footnote 15) When shown as present values, future year impacts have been discounted at 3% per year to 2017 (the year of the analysis), as per TBS guidance.

Updates to the analysis following the publication of the proposed Amendments in the Canada Gazette, Part I (CG-I)

Various updates were made to the analysis following the publication of the proposed Amendments in the Canada Gazette, Part I. As a result of these modifications, the estimated costs attributable to the Amendments have increased from $686 million to $2,236 million, while the estimated benefits have changed from $6,787 million to $6,239 million. The change in these estimates is due largely to updated information received from stakeholders through consultations after the CG-I comment period. However, the Department’s updated analysis indicates that the Amendments will result in significant net benefits. The updates to the analysis are discussed below.

Regulatory updates: Based on the comments received following the publication of the proposed Amendments in the Canada Gazette, Part I, minor modifications have been made to the Amendments. The Global Warming Potential thresholds have been amended for centralized refrigeration systems, chillers, and stand-alone medium temperature refrigeration systems. Additionally, the phase-down schedule has been amended to ensure Canada’s obligations under the Kigali Amendment are met. The analysis has therefore been updated to account for these changes, which are expected to have negligible impacts.

Consultation updates: Comments received following the publication of the proposed Amendments included feedback from stakeholders regarding the Regulatory Impact Analysis Statement. Most notably, comments were made regarding the accuracy of price estimates of alternative substances assumed to replace HFCs and the feasibility of assumed alternatives. In reaction to these comments the following substantive changes have been made to the assumptions, which have led to changes in the results: (a) prices of alternatives, particularly HFOs and blends containing them, have been revised upward; (b) the assumed alternative for extruded polystyrene (XPS) foam has been changed from hydrocarbons to HFO-1234ze leading to increased costs due to higher blowing agent prices; and (c) only the largest supermarkets are now assumed to install “transcritical” CO2 systems. Additionally, the incremental capital cost of these systems has been revised upward.

General updates: The modifications to the analysis include updating price levels, exchange rates, substance prices and projections of baseline HFC consumption to align with the most up-to-date information. The base year used to discount costs and benefits to present value has been updated to 2017.

Analysis of regulatory coverage and compliance

To estimate the incremental benefits and costs of the Amendments, the analysis considered who will be affected (regulatory coverage) and how they will most likely respond (their compliance strategies), as described below.

Regulatory coverage

Several industry groups that use HFCs will either be directly or indirectly affected by the Amendments; others are not expected to be affected in a material way.

HFC recyclers and reclaimers: These will not be directly regulated nor will they be affected. Federal and provincial governments have initiatives to mandate and encourage the responsible management of recovered HFCs. This will increase the supply of HFCs, as HFCs from retired equipment are recovered and subsequently recycled or reclaimed. These quantities of recycled/reclaimed HFCs could be used to service existing equipment in years in which demand for HFCs exceeds the quantity of virgin HFCs that can be imported. These recycled/reclaimed quantities were not considered in this analysis, as it is expected that imported HFCs necessary to service and maintain legacy equipment will be available in sufficient quantities.

Companies servicing new equipment with HFC alternatives: These will not be directly regulated but will be required to obtain alternative substances. In cases where equipment requires regular maintenance, it is expected that any incremental maintenance costs due to higher alternative substance prices will be passed on to end-users.

Importers of HFC-containing products: These will be regulated, but it is expected they will not be affected. It is assumed products manufactured outside of Canada will be already meeting the product-specific standards in the absence of the Amendments, as they will likely need to meet similar regulatory measures already in place in the United States, European Union, and Japan. Therefore, it is expected there will be no incremental impacts from imported manufactured goods.

Importers of bulk HFCs: These will be regulated and will need to reduce the quantity of imported HFCs. It is expected that the import of specific alternative substances will be driven by demand from manufacturers and end-users, and any costs due to higher substance prices will be passed on to these groups.

Manufacturers of products containing HFCs: The manufacturers within each sub-sector will be regulated and will transition to alternative substances with Global Warming Potentials below the required threshold, being motivated by product-specific controls and a reduced availability of HFCs due to the bulk phase-down. Table 2 below outlines the primary characteristics of the affected sub-sectors as well as the Global Warming Potential thresholds under the product-specific controls and the coming-into-force dates.

Table 2: Description and product-specific controls by end-use

| End-use |

Description |

Global Warming Potential Threshold |

Coming into Force |

|---|---|---|---|

Stand-alone refrigeration |

Stand-alone refrigeration systems use HFCs as refrigerants in self-contained systems generally used in supermarkets and convenience stores to store and display perishable foods, beverages and frozen foods. |

1 400 1 500 |

2020 |

Centralized refrigeration |

Centralized refrigeration systems are generally used for storing and displaying food, beverages, and other perishables in convenience stores and supermarkets, using HFCs as refrigerants. |

2 200 |

2020 |

Chillers |

Chillers using HFCs as refrigerants are generally used to provide air-conditioning for large commercial buildings or refrigeration in industrial settings. |

750 |

2025 |

Mobile refrigeration |

Mobile refrigeration systems use HFCs as refrigerants to provide refrigeration during the shipping of food and beverage products (e.g. refrigerated trucks). |

2 200 |

2025 |

Domestic air conditioning |

Domestic air conditioners use HFCs as refrigerants and are found in residential and small commercial buildings. |

Not applicable |

|

Domestic refrigeration |

There are no known domestic manufacturers of domestic refrigeration equipment in Canada. |

150 |

2025 |

Extruded polystyrene (XPS) foam |

HFCs with a Global Warming Potential of 1 430 are used as a blowing agent in the manufacture of XPS foam used for wall, roof, and floor insulation. (see footnote 16) |

150 |

2021 |

Rigid polyurethane (PU) foam |

HFCs are used as blowing agents in rigid PU foam products in the manufacture of insulation products for appliances, pipes, and buildings. |

150 |

2021 |

High pressure polyurethane spray foam |

HFCs are used as a blowing agent in high pressure PU spray foam products for the installation of wall, roof, and floor insulation. |

150 |

2021 |

Low pressure polyurethane spray foam |

HFCs are used as a blowing agent in low pressure PU spray foam products for the installation of wall, roof, and floor insulation. |

150 |

2021 |

Motor vehicle air-conditioning (MVAC) |

Motor vehicle air-conditioners typically contain HFCs as refrigerants. |

150 |

2021 model year vehicles |

Aerosols |

HFCs are used in aerosol products as propellants in a range of personal care, household, and cleaning products. |

150 |

2018 |

Compliance strategies for manufacturers of products with HFCs

As bulk importers comply with the phase-down schedule in the Amendments, the annual supply of HFCs for domestic consumption will be reduced. As manufacturers comply with the product-specific controls on HFC use in the Amendments, they are also expected to respond to the reduced supply of HFCs. Both the regulatory controls on HFC-containing products and the reduced supply of HFCs will encourage manufacturers to choose alternatives with lower Global Warming Potentials.

In choosing alternatives that comply with the Amendments, manufacturers of products with HFCs will have to consider technical feasibility, safety, and economic feasibility. For the purposes of this analysis, the alternative substances assumed to replace HFCs for each end-use were selected based on three main criteria:

Technical feasibility: The substance is a technically feasible alternative with the chemical properties needed for the specific end-use.

Safety: The alternative substance has been proven to be safe to use in a given application. Some alternatives to HFCs are flammable, and precautions must be taken when in use for safety reasons. These alternatives include hydrocarbons such as propane. However, flammable refrigerants and foam blowing agents can be used in systems and products designed for them. When possible, it is assumed that alternatives with similar flammability properties to the HFC being replaced will be chosen. Alternatives with higher flammability have only been chosen in cases where they have been proven to be safe for use.

Economic feasibility: The relative costs of potential alternatives and the associated capital costs were assessed for substances that were both technically feasible and safe for use. From the set of feasible alternatives, it is assumed that the least costly alternative will be chosen, unless industry consultation has stated otherwise.

When determining likely strategies to comply with the product-specific controls and the bulk HFC phase-down, domestic consumption of HFCs and alternatives are modelled in two steps:

- Manufacturers of products subject to product-specific controls (grouped by “end-use”) are assumed to use an alternative substance below the required product-specific Global Warming Potential limits in the same quantities. Products manufactured with these alternative substances will then be serviced and maintained with the same substances.

- In the years in which reductions of HFC use (in CO2e) from the product-specific controls alone are insufficient to meet the bulk phase-down requirements, it is assumed each end-use will further reduce HFC use by the same proportion. To achieve these reductions, some manufacturers will transition production to an alternative with a lower Global Warming Potential than that used to comply with these controls. (see footnote 17) In certain cases where the reduction in CO2e from transitioning to the first phase-down alternative is insufficient to meet the phase-down schedule, a second phase-down alternative is used. It is assumed that substances are imported in quantities to meet demand from manufacturers and servicing, subject to the supply constraint imposed by the phase-down. Therefore, the impacts of the phase-down are attributed to manufacturers and end-users of HFC-containing products.

The alternative assumptions in this analysis were determined for the purposes of quantifying compliance costs and GHG reductions. These assumptions are not intended to represent the entirety of available alternatives, or to imply that other viable alternatives cannot or should not be used. For the purposes of modelling, the phase-down was assumed to affect all sub-sectors proportionately. In reality, it is likely that some sub-sectors and certain small businesses will have more challenges than others in transitioning to low-Global Warming Potential alternatives. Therefore, the reductions will not be equally distributed.

Table 3: Compliance assumptions for the baseline and regulatory scenario: product-specific controls

| End-use |

Baseline Scenario |

Product-specific Controls Alternative (Global Warming Potential) |

Phase-down |

Phase-down |

|---|---|---|---|---|

Stand-alone refrigeration |

R-404A/R-507A (3 922/3 985) |

R-290 (propane) (3) |

No Change (3) |

N/A |

R-448A/R-449A (1 387) |

R-455A/R-454C (148) |

N/A |

||

R-407A (2 107) |

R-290 (propane) (3) |

No Change (3) |

N/A |

|

HFC-134a (1 430) |

R-290 (propane) (3) |

No Change (3) |

N/A |

|

Centralized refrigeration (87% of total volume) |

R-404A/R-507A (3 922/3 985) |

R-407A (2 107) |

R-448A/R-449A (1387) |

HFO/HFC Blend (<300) |

R-407A (2 107) |

No Change (2 107) |

|||

HFC-134a (1 430) |

No Change (1 430) |

R-450A/R-513A (604/631) |

HFO/HFC Blend (<300) |

|

Centralized refrigeration (13% of total volume) |

R-404A/R-507A (3 922/3 985) |

R-407A (2 107) |

R-744 (CO2) (1) |

N/A |

R-407A (2 107) |

No Change (2 107) |

|||

HFC-134a (1 430) |

No Change (1 430) |

|||

Chillers |

HFC-134a (1 430) |

R-450A/R-513A (604/631) |

HFO-1234ze (6) |

N/A |

HFC-245fa (1 030) |

HFO-1233zd/ |

No Change (1 387) |

N/A |

|

R-407C (1 774) |

R-450A/R-513A (604/631) |

No Change (604/631) |

N/A |

|

R-404A/R-507A (3 922/3 985) |

R-448A/R-449A (1387) |

No Change (1 387) |

N/A |

|

Mobile refrigeration |

R-404A/R-507A (3 922/3 985) |

R-452A (2 140) |

R-448A/R-449A (1 387) |

HFO/HFC Blend (<300) |

Domestic air conditioning |

R-410A (2 088) |

Not Affected by Product-Specific Controls |

R-32 (675) |

HFO/HFC Blend (<300) |

R-407C (1 774) |

||||

Domestic refrigeration |

Not manufactured in Canada |

|||

Extruded polystyrene foam |

HFC-134a (1 430) |

R-450A (604) |

HFO-1234ze (6) |

N/A |

Rigid polyurethane foam |

HFC-245fa (1 030) |

HFO-1233zd/ HFO-1336mzz (5/9) |

No Change |

N/A |

HFC-365mfc/227ea (1 150) |

HFO-1233zd/ |

No Change |

N/A |

|

High pressure polyurethane spray foam |

HFC-245fa (1 030) |

HFO-1233zd/ HFO-1336mzz (5/9) |

No Change |

N/A |

HFC-365mfc/227ea (1 150) |

HFO-1233zd/ HFO-1336mzz (5/9) |

No Change |

N/A |

|

Low pressure polyurethane spray foam |

HFC-134a (1 430) |

R-450A (604) |

HFO-1234ze (6) |

N/A |

Motor vehicle air-conditioning (MVAC) |

HFC-134a (1 430) (Prior to 2021) |

HFCs not expected to be used post-2021 |

HFO-1234yf (4) |

N/A |

Aerosols |

HFC-152a (124) |

No Change (124) |

HFO (6) |

N/A |

Note: Subsectors which are assumed to transition to an alternative that does not contain HFCs to comply with the product-specific controls are not affected by the phase-down. |

||||

In specific cases, the choice of alternatives will depend on the size of the facility. The largest supermarkets (about 1 100 stores over the period of analysis) are assumed to transition to transcritical CO2 systems, which require large upfront capital costs, in response to a decreased supply of R-407A. (see footnote 18) Most supermarkets are expected to respond to the bulk phase-down by transitioning to HFO/HFC blends, such as R-448A or R-449A, to avoid these capital costs.

Chiller manufacturers, with the exception of a small number of low-pressure centrifugal chiller manufacturers (using HFC-245fa), are expected to transition to substances containing HFCs to comply with the product-specific controls. However, due to uncertainty surrounding secondary alternatives for some cases, only manufacturers currently using HFC-134a are assumed to be affected by the phase-down.

Domestic air-conditioning manufacturers are assumed to transition to R-32. Although R-32 is a mildly flammable refrigerant, it has been safely used in domestic air-conditioning units in other countries. (see footnote 19) However, safety standards in Canada would need to be amended to allow its use. For the purposes of this analysis, it is assumed this change will take place as it would be consistent with regulatory safety regimes in other countries. The domestic air-conditioning sector is not expected to be significantly affected until 2024, leaving adequate time to amend these standards, if appropriate.

Due to existing provisions in the Passenger Automobile and Light Truck Greenhouse Gas Emission Regulations, motor vehicle manufacturers are expected to have completely phased out HFC use by model year 2021. Adoption of HFO-1234yf is expected to increase relative to the baseline for 2019 and 2020 model year vehicles due to the bulk phase-down, thus resulting in incremental costs and benefits attributable to the Amendments. The product-specific controls, which come into effect in 2021, are not expected to result in incremental costs or benefits.

GHG emission reduction benefits

The Amendments will phase down bulk imports of HFCs and control the use of HFCs in specified products that contain them, both reducing the supply of HFCs and restricting their use by product manufacturers. As the manufacturing of products containing HFCs shifts to HFC alternatives with lower Global Warming Potential, a reduction in GHG emissions (in CO2-equivalent) from HFCs is expected.

GHG emissions modelling

Historic HFC quantities for each end-use are estimated using bulk HFC import volume data and in-product HFC survey data. Future HFC use is then projected forward using the Department of Finance Canada’s gross domestic product growth rates, taking into consideration the continued replacement of phased-out HCFCs with HFC substitutes. The baseline scenario does not take into consideration the future adoption of recently introduced low Global Warming Potential alternatives, such as hydrofluoroolefins (HFOs), which may be adopted by domestic manufacturers in the absence of the Amendments.

To estimate future emissions attributable to HFC use, baseline leak rates were applied to estimated future quantities of HFCs used. Each end-use was assigned three life phases, with associated leak rates for each life phase: assembly, usage, and end-of-life disposal. These leak rates were developed from a survey performed by Environmental Health Strategies Inc.; they were then finalized in accordance with the quality control and verification guidelines of the Intergovernmental Panel on Climate Change (IPCC).

The Global Warming Potential for each HFC substance is used in order to calculate its CO2 equivalence (CO2e). Consistent with IPCC guidance, these CO2e estimates are calculated using a 100-year time frame for each HFC substance. (see footnote 20) Global Warming Potential estimates were provided by the IPCC in its Fourth Assessment Report and have been used in this analysis.

The baseline estimates are consistent with the Department’s National Inventory Report and Canada’s 2016 Greenhouse Gas Emissions Reference Case. (see footnote 21), (see footnote 22) The following data sources were used to project future HFC consumption and the resultant emissions:

- Environment and Climate Change Canada — Bulk HFC import section 71 survey data (2008–2015);

- Environment and Climate Change Canada — In-product HFC survey data (2005–2010); and

- Environment and Climate Change Canada — National Inventory Report (1990–2015).

This same emission estimation process was applied to the regulatory scenario, with the same leak rates and life-cycle assumptions. Therefore, emission reductions attributable to the Amendments are driven by the reduction in Global Warming Potential of the substances used in the regulatory scenario.

GHG emission results

The Amendments will reduce emissions of the HFCs with the largest climate impacts by requiring their replacement with alternatives that have lower Global Warming Potentials. The cumulative incremental GHG emission reductions are estimated to be approximately 168 Mt CO2e over the time frame of analysis (2018–2040), a 34% decrease relative to the baseline scenario.

The Department’s central estimate of the social cost of carbon (SCC) was used to estimate the monetized value of reducing CO2e emissions under the Amendments. The SCC represents an estimate of the economic value of avoided climate change damages at the global level for current and future generations as a result of reducing CO2 emissions. The incremental GHG reductions (in megatonnes CO2e) for each year were valued using annual SCC values (in 2016 dollars per tonne of CO2e) over the time frame of analysis. These SCC values increase over time, from $45 in 2018 to $67 in 2040 per tonne of CO2e. (see footnote 23) This method may underestimate the benefits of reducing SLCPs, such as HFCs, which have greater climate impacts (in present value terms) than those derived using CO2e estimates based on 100-year Global Warming Potentials.

The central SCC value used in this cost-benefit analysis may not fully capture potential low-probability, high-impact outcomes due to climate change. To address this concern, the Department publishes a 95th percentile SCC value for sensitivity analyses, which attempts to capture the costs associated with low-probability, high-impact outcomes, including potential catastrophic impacts of climate change. (see footnote 24)

Table 4: Incremental GHG emission reductions (in megatonnes CO2e and in millions of dollars)

2018 to 2020 |

2021 to 2025 |

2026 to 2030 |

2031 to 2035 |

2036 to 2040 |

Total |

|

|---|---|---|---|---|---|---|

GHG emission reductions (Mt CO2e) |

2 |

10 |

24 |

52 |

79 |

168 |

Present value of GHG emission reductions — Central case SCC |

86 |

437 |

953 |

1,949 |

2,766 |

6,191 |

Note: Totals may not sum due to rounding. |

||||||

For the purposes of this analysis, emission reductions are quantified and monetized up to 2040. However, there will be emission reductions beyond 2040 attributable to industry actions with upfront costs incurred before 2040, as emissions occur throughout the useful life of HFC-containing products.

Contribution to Paris Agreement commitment (emission reductions in 2030)

Canada has made commitments to reduce GHG emissions by 30% below 2005 levels by 2030 under the Paris Agreement. The Department estimates that annual emission reductions of 219 Mt CO2e will be required in 2030 to deliver on this commitment. GHG reductions from the Amendments (7 Mt) will deliver a 3% contribution to Canada’s GHG emissions reduction target (219 Mt) under the Paris Agreement. (see footnote 25)

For the Amendments, the cumulative GHG emission reductions between 2018 and 2030 are estimated to be 37 Mt CO2e (due to rounding, the values in Table 4 only add to 36). Without the Amendments, annual GHG emissions from HFCs in Canada were projected to increase from 9 Mt CO2e in 2014 to 19 Mt in 2030. GHG emission reductions attributable to the Amendments are expected to reach 7 Mt in 2030, reducing HFC emissions to 12 Mt. (see footnote 26)

Contribution to Pan-Canadian Framework

The Pan-Canadian Framework was developed to establish a comprehensive plan to meet Canada’s commitments under the Paris Agreement. The Pan-Canadian Framework proposed a range of complementary climate actions to support pricing carbon pollution in reducing GHG emissions. The Amendments are one such measure that reduce GHG emissions in a complementary fashion to carbon pricing mechanisms, as these measures do not cover most HFC emissions.

Costs (and cost savings)

Compliance with the Amendments will lead to incremental costs and cost savings to industry. Adopting HFC alternatives will lead to changes in substance costs and, in some cases, capital costs to allow the use of these alternatives. Using HFC alternatives may be more or less expensive than using HFCs, resulting in an operating cost or savings, and may require changes in products or equipment, resulting in a capital cost.